Introduction to Client Due Diligence (CDD)

Customer due diligence (CDD) is a crucial part of compliance for UK law firms. It involves the process of identifying and verifying the identity of clients, assessing the risks associated with them, and monitoring their activities. CDD is mandated by the Solicitors Regulation Authority (SRA) as part of its regulatory framework, and non-compliance can result in serious consequences for law firms. In this blog post, we will provide a comprehensive CDD checklist for UK law firms, with guidance from the SRA, Law Society of England and Wales, and the Legal Sector Affinity Group (LSAG).

Mitigating the risk of money laundering and terrorist financing

Compliance with CDD regulations is essential for UK law firms to mitigate the risk of money laundering and terrorist financing. The SRA, Law Society, and LSAG provide guidance on best practices for CDD, including the steps outlined in this checklist. By implementing these procedures and regularly reviewing and updating them, law firms can ensure that they are meeting their regulatory obligations and protecting themselves and their clients from financial crime.

SRA Regulations

The SRA’s regulations on CDD can be found in its Code of Conduct for Solicitors, RELs and RFLs. Regulation 33 requires law firms to have risk assessments in place, while Regulation 18.1 requires the verification of client identity before providing any services. Regulation 21.1 requires law firms to ensure that any proposed transaction is legal and legitimate.

LSAG Guidance

The Legal Sector Affinity Group (LSAG) is a collaboration of UK government agencies and professional bodies, including the SRA and the Law Society. LSAG provides guidance on best practices for CDD, including suspicious activity reporting and risk assessments. Their guidance can be found on their website.

Law Society Guidance

The Law Society of England and Wales provides guidance on CDD for its members. Their guidance includes best practices for client identification and verification, risk assessments, and ongoing monitoring. The Law Society also provides guidance on the types of documents that can be used for client identification and verification.

Client Identification and Verification

The Law Society’s guidance on client identification and verification includes best practices for obtaining original documents, using independent sources, and verifying the authenticity of documents. The guidance also provides examples of documents that can be used for verification, such as passports and driving licenses.

Risk Assessments

The Law Society’s guidance on risk assessments includes best practices for assessing the risk associated with clients and transactions. This includes understanding the client’s risk profile, the nature of the relationship, and the source of funds or wealth. The guidance also provides examples of risk factors that law firms should consider when conducting risk assessments.

Ongoing Monitoring

The Law Society’s guidance on ongoing monitoring includes best practices for reviewing and updating client information, monitoring for suspicious activity, and reporting any suspicious activity to the relevant authorities. The guidance also provides examples of suspicious activity and best practices for reporting.

Verification of Source of Funds or Wealth

The Law Society’s guidance on the verification of the source of funds or wealth includes best practices for obtaining information on the client’s financial history, income sources, and any potential conflicts of interest. The guidance also provides examples of documents that can be used for verification, such as bank statements and tax returns.

Beneficial Ownership

The Law Society’s guidance on beneficial ownership includes best practices for understanding the ownership structure, any trusts or nominee arrangements, and any third parties involved. The guidance also provides examples of documents that can be used for verifying beneficial ownership.

Documentation and Record Keeping

The Law Society’s guidance on documentation and record keeping includes best practices for maintaining records of client identification and verification, risk assessments, transaction details, and any supporting documentation. The guidance also provides examples of the types of records that law firms should retain and for how long.

Compliance with CDD regulations is essential

Compliance with CDD regulations is essential for UK law firms to protect themselves and their clients from financial crime. The SRA, LSAG, and Law Society provide guidance on best practices for CDD, including client identification and verification, risk assessments, ongoing monitoring, and record keeping. By following these best practices and regularly reviewing and updating their procedures, law firms can ensure that they are meeting their regulatory obligations and reducing the risk of money laundering and terrorist financing.

Benefits of CDD Compliance

Compliance with CDD regulations not only helps law firms meet their regulatory obligations, but it also has several other benefits.

These include:

* Protecting the firm’s reputation and brand by demonstrating a commitment to ethical business practices.

* Building trust and confidence with clients by demonstrating a commitment to their safety and security.

* Reducing the risk of financial loss or penalties from non-compliance.

* Identifying potential risks and vulnerabilities in the firm’s operations, allowing for early intervention and mitigation.

* Improving operational efficiency and reducing costs by streamlining processes and eliminating unnecessary steps.

Step by Step guide to Client Due Diligence

Step 1: Identify the client

The first step in CDD is to identify the client and establish the nature of the relationship. This includes determining the legal entity, beneficial ownership, and any third parties involved. The SRA requires law firms to obtain and verify the client’s identity before providing any services.

Step 2: Verify the client’s identity

The SRA mandates that law firms must verify the client’s identity using reliable and independent sources. This includes obtaining original documents such as passports, driving licenses, or national identity cards. The Law Society provides guidance on the types of documents that can be used for verification, such as those with biometric data and holograms.

Step 3: Assess the risk

The next step in CDD is to assess the risk associated with the client and the transaction. The SRA requires law firms to have risk assessments in place to determine the level of due diligence required. This includes assessing the client’s risk profile, the nature of the relationship, and the source of funds or wealth.

Step 4: Conduct ongoing monitoring

Law firms must conduct ongoing monitoring of their clients and transactions to ensure compliance with CDD regulations. This includes regularly reviewing and updating client information, and monitoring for any suspicious activity. The LSAG provides guidance on suspicious activity reporting and best practices for monitoring.

Step 5: Determine the purpose of the transaction

Law firms must determine the purpose of the transaction and the expected outcome. This includes understanding the client’s objectives and any potential risks or challenges. The SRA requires law firms to ensure that any proposed transaction is legal and legitimate.

Step 6: Obtain information on the source of funds or wealth

The SRA requires law firms to obtain information on the source of funds or wealth for any transaction. This includes understanding the client’s financial history, income sources, and any potential conflicts of interest. The Law Society provides guidance on best practices for obtaining this information.

Step 7: Verify the source of funds or wealth

Law firms must verify the source of funds or wealth to ensure that they are legitimate and not the proceeds of crime. This includes obtaining supporting documentation such as bank statements, tax returns, or business records. The SRA provides guidance on the types of documents that can be used for verification.

Step 8: Determine the beneficial owner

Law firms must determine the beneficial owner of the transaction and verify their identity. This includes understanding the ownership structure, any trusts or nominee arrangements, and any third parties involved. The SRA requires law firms to ensure that they have identified and verified the beneficial owner of the transaction.

Step 9: Review the risk assessment

Law firms must regularly review and update their risk assessments based on any changes to the client or transaction. This includes re-assessing the risk profile, verifying client information, and monitoring for any suspicious activity. The LSAG provides guidance on best practices for risk assessment and ongoing monitoring.

Step 10: Document and retain records

Law firms must document and retain records of their CDD procedures and outcomes. This includes maintaining records of client identification and verification, risk assessments, transaction details, and any supporting documentation. The SRA requires law firms to retain these records for a minimum of five years after the end of the business relationship.

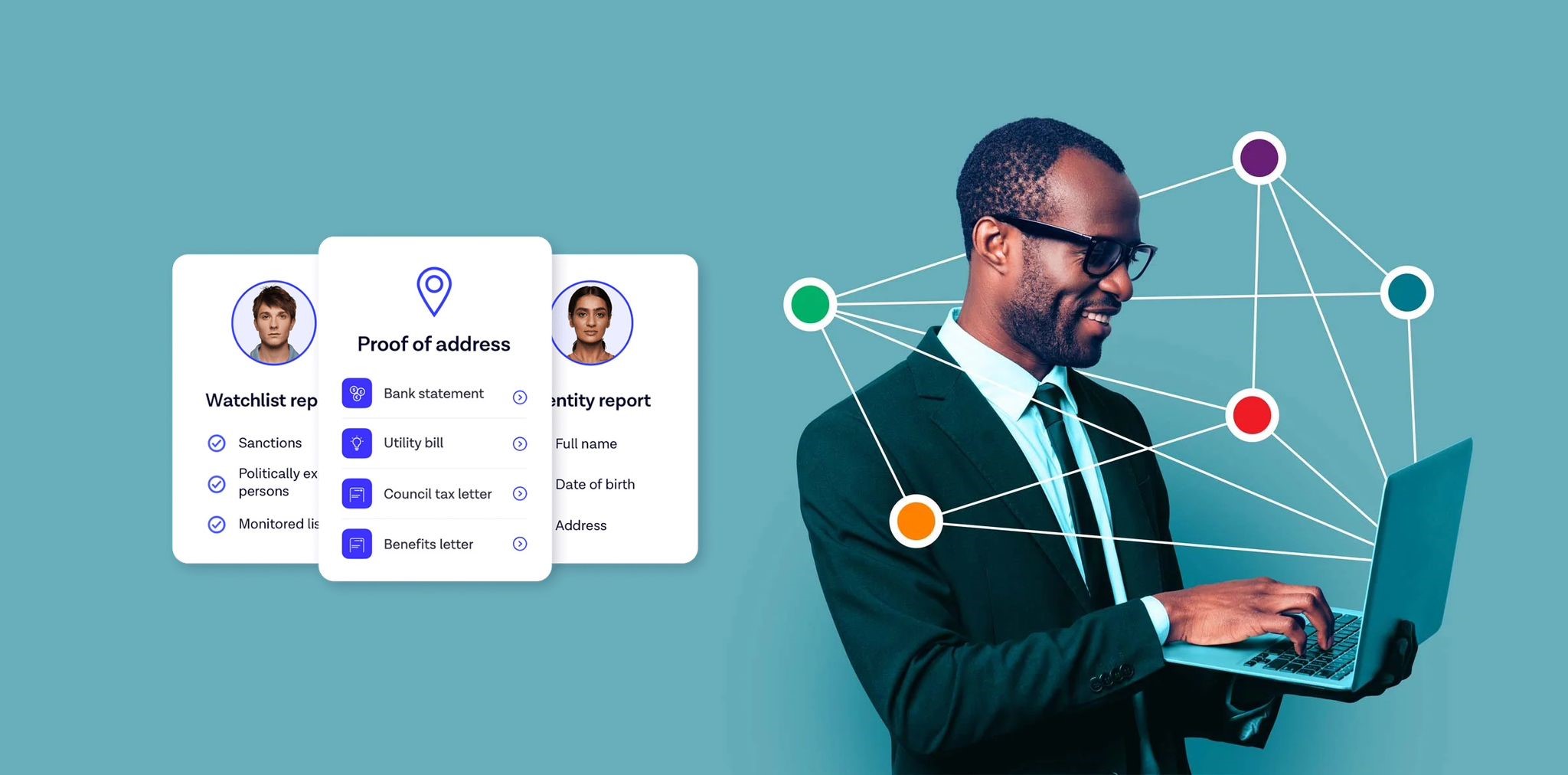

Technology Solutions for AML Compliance & Client Due Diligence

Technology can also play a critical role in helping law firms comply with CDD regulations. One such solution is Verify 365, a digital client onboarding platform designed specifically for the legal sector.

Verify 365 automates the client identification and verification process, enabling law firms to:

* Verify client identities in real-time using a range of independent sources and databases.

* Conduct risk assessments and verify the source of funds or wealth.

* Collect and store client data securely, reducing the risk of data breaches.

* Streamline the onboarding process, reducing the time and resources required.

* Ensure compliance with CDD regulations and reduce the risk of financial crime.

Verify 365 also integrates with other legal technology solutions, such as case management systems and document management systems, to provide a seamless end-to-end solution for law firms.

Compliance with CDD regulations is essential for UK law firms to protect themselves and their clients from financial crime. The SRA, LSAG, and Law Society provide guidance on best practices for CDD, including client identification and verification, risk assessments, ongoing monitoring, and record keeping. By following these best practices and leveraging technology solutions such as Verify 365, law firms can ensure that they are meeting their regulatory obligations and reducing the risk of money laundering and terrorist financing.